All Categories

Featured

Table of Contents

In my viewpoint, Claims Paying Ability of the carrier is where you base it. You can look at the state warranty fund if you desire to, yet bear in mind, the annuity mafia is enjoying.

They understand that when they put their cash in an annuity of any kind, the business is going to back up the claim, and the industry is overseeing that. Are annuities guaranteed? Yeah, they are - an immediate annuity may be purchased with. In my viewpoint, they're risk-free, and you need to go right into them checking out each provider with confidence.

3 Year Fixed Annuities

If I placed a recommendation in front of you, I'm likewise putting my license on the line. Bear in mind that (annuities trusts). I'm very certain when I placed something in front of you when we chat on the phone. That doesn't mean you have to take it. You might claim, "Yes, Stan, you claimed to buy this A-rated business, but I really feel much better with A double and also." Fine.

We have the Claims Paying Ability of the carrier, the state guaranty fund, and my close friends, that are unknown, that are circling around with the annuity mafia. That's a valid answer of somebody that's been doing it for a very, extremely long time, and that is that a person? Stan The Annuity Male.

Individuals normally purchase annuities to have a retired life income or to develop financial savings for an additional purpose. You can acquire an annuity from a licensed life insurance policy representative, insurance coverage company, financial planner, or broker - rate of return on annuities. You ought to talk with a monetary adviser about your needs and objectives before you acquire an annuity

The difference in between the 2 is when annuity settlements start. You do not have to pay tax obligations on your profits, or contributions if your annuity is an individual retired life account (INDIVIDUAL RETIREMENT ACCOUNT), until you take out the earnings.

Deferred and prompt annuities offer a number of alternatives you can select from. The choices offer various degrees of potential threat and return: are ensured to earn a minimal rate of interest. They are the most affordable economic danger however provide reduced returns. gain a higher rates of interest, however there isn't an ensured minimum interest price.

Annuity Cash In Value

permit you to select in between sub accounts that are similar to mutual funds. You can gain a lot more, however there isn't an assured return. Variable annuities are higher threat due to the fact that there's an opportunity you might shed some or all of your money. Fixed annuities aren't as dangerous as variable annuities since the financial investment danger is with the insurance provider, not you.

If efficiency is reduced, the insurance provider bears the loss. Fixed annuities ensure a minimum rate of interest price, generally between 1% and 3%. The business may pay a higher interest price than the guaranteed interest rate - best deferred annuity. The insurance provider figures out the rate of interest, which can alter regular monthly, quarterly, semiannually, or each year.

Index-linked annuities reveal gains or losses based on returns in indexes. Index-linked annuities are extra intricate than repaired deferred annuities. It is essential that you comprehend the attributes of the annuity you're taking into consideration and what they suggest. The two contractual functions that affect the quantity of interest credited to an index-linked annuity one of the most are the indexing approach and the involvement rate.

Each counts on the index term, which is when the business computes the passion and credits it to your annuity (annuities 101). The figures out just how much of the boost in the index will be utilized to determine the index-linked rate of interest. Other crucial functions of indexed annuities include: Some annuities cap the index-linked rates of interest

Not all annuities have a floor. All fixed annuities have a minimum surefire value.

Other annuities pay compound interest throughout a term. Compound interest is passion gained on the cash you saved and the interest you earn.

How Do You Get An Annuity

If you take out all your money prior to the end of the term, some annuities will not attribute the index-linked interest. Some annuities might credit only component of the passion.

This is because you bear the financial investment danger rather than the insurer. Your representative or monetary adviser can help you choose whether a variable annuity is right for you. The Securities and Exchange Payment categorizes variable annuities as protections because the performance is derived from supplies, bonds, and various other investments.

Annuity With Highest Interest Rates

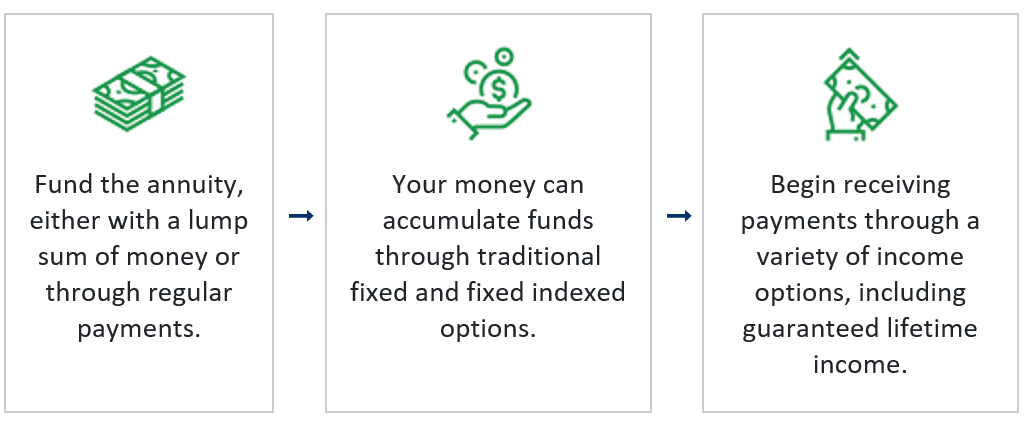

Discover more: Retirement ahead? Consider your insurance policy. An annuity contract has two stages: an accumulation phase and a payment stage. Your annuity gains passion throughout the build-up stage. You have a number of choices on just how you add to an annuity, depending upon the annuity you acquire: allow you to pick the moment and amount of the payment.

allow you to make the exact same repayment at the exact same interval, either monthly, quarterly, or annually. The Internal Earnings Service (INTERNAL REVENUE SERVICE) regulates the taxes of annuities. The internal revenue service enables you to postpone the tax obligation on profits till you withdraw them. If you withdraw your earnings before age 59, you will probably need to pay a 10% very early withdrawal charge in enhancement to the taxes you owe on the rate of interest earned.

Annuity Payment Meaning

After the build-up stage finishes, an annuity enters its payout phase. There are a number of choices for getting settlements from your annuity: Your firm pays you a fixed quantity for the time specified in the agreement.

Numerous annuities bill a fine if you withdraw money before the payout stage - learn about annuity. This charge, called an abandonment fee, is generally greatest in the very early years of the annuity. The charge is commonly a percentage of the taken out cash, and normally begins at around 10% and drops annually up until the surrender period is over

{kind=link}

Table of Contents

Latest Posts

Exploring Tax Benefits Of Fixed Vs Variable Annuities Key Insights on Your Financial Future Breaking Down the Basics of Investment Plans Pros and Cons of Annuity Fixed Vs Variable Why Indexed Annuity

Decoding Immediate Fixed Annuity Vs Variable Annuity Key Insights on Your Financial Future Breaking Down the Basics of Pros And Cons Of Fixed Annuity And Variable Annuity Benefits of Fixed Vs Variable

Breaking Down Variable Annuities Vs Fixed Annuities A Comprehensive Guide to Fixed Vs Variable Annuity Pros And Cons What Is the Best Retirement Option? Advantages and Disadvantages of Variable Annuit

More

Latest Posts